BUSINESS

5 Benefits Of Working With A Cpa For Estate Planning

Estate planning can feel heavy. You work hard, save what you can, and want to leave clear support for the people you love. Yet tax rules, changing laws, and complex forms create fear and confusion. A CPA helps you cut through that noise. You get clear answers, straight numbers, and a plan that matches your real life. An East Brunswick CPA can help you understand how your house, savings, retirement accounts, and business pass on to others. You also see how taxes may affect each choice. This support reduces conflict, protects your wishes, and helps your family avoid sudden stress. You do not need to guess. You do not need to go through this alone. Working with a CPA gives you structure, control, and calm. The next sections explain five specific benefits you can expect.

1. You lower tax shocks for your family

Estate planning is about more than who gets what. It is about what is left after taxes. Without a plan, your family can face surprise bills and delays. A CPA helps you see the tax impact of each decision before you sign anything.

You learn how federal estate and gift tax rules work in plain terms. For example, the IRS explains current estate and gift tax limits and how they change over time on its Estate and Gift Taxes page. A CPA uses this public guidance and applies it to your life.

You and your CPA can review three key questions.

- What taxes may apply to your house, savings, and retirement accounts

- How to use lifetime gifts in a smart way

- How to time transfers so your loved ones keep more

This careful review does not erase all tax. It reduces shock and waste.

2. You turn a confusing process into clear steps

Estate planning feels confusing because it mixes money, law, and family ties. A CPA helps you turn that confusion into a simple checklist.

You start with what you own. You list your home, other property, bank accounts, retirement funds, life insurance, and any business interests. Next you list who depends on you. Children. A spouse. Aging parents. A relative with a disability. Then you match your assets to your goals.

A CPA works with your attorney and other advisors. You get one joined plan instead of scattered documents. The American Bar Association stresses how tax and legal advice work together in its public guidance on estate planning at americanbar.org. A CPA helps you stand in the middle of that team.

By the end, you have three things.

- A written summary of your assets and debts

- A clear list of who should receive what

- A schedule to review and update your plan

This simple structure reduces fear and helps your family know what to expect.

3. You protect small details that matter later

Small details often cause the biggest fights. A missed form. An outdated name on an account. A forgotten loan. A CPA pays close attention to these details because the cost of one mistake can be high.

Here are three common problem points a CPA helps you fix.

- Beneficiary forms on retirement accounts and life insurance

- Titles on property and bank accounts

- Old wills that do not match your current wishes

A CPA helps you check that your beneficiary forms match your will. You also check that account titles match your plan. You look at old tax returns to spot assets you might forget. This quiet work protects your family from court fights and delays.

4. You plan for long term care and special needs

Estate planning is not only about what happens after you die. It is also about what happens if you cannot speak for yourself. A CPA helps you think about long term care, disability, and special needs without turning away from the pain.

You look at questions like these.

- If you need care, what resources will pay for it

- How will that care affect what you leave your family

- Does anyone you love need extra protection for special needs

For example, a child with special needs might lose public benefits if they receive money the wrong way. A CPA can work with your attorney to support tools like special needs trusts and clear funding plans. You do not only leave money. You leave structure and care.

5. You keep your plan current as life changes

Your life changes. Your plan must change too. Birth, death, divorce, job loss, new business, or a move to another state can all affect your estate plan. Tax rules also change on a regular cycle. A plan you sign once and forget can cause harm later.

A CPA helps you set a review schedule. Many people choose every two or three years. Some need yearly reviews when they own a business or large assets. During each review you check three things.

- Your family list and your chosen heirs

- Your asset list and how each item passes at death

- Recent tax law changes that may affect your plan

This cycle keeps your plan current. It also gives your family a known contact who understands your full picture.

Example comparison of planning with and without a CPA

| Planning task | Without CPA | With CPA

|

|---|---|---|

| Identify all assets and debts | Self made list that may miss accounts or loans | Structured review using tax returns and statements |

| Estimate tax impact | Guess based on online tools | Specific estimates based on current IRS rules |

| Coordinate with attorney | Separate talks that may conflict | Aligned plan with shared documents and goals |

| Update schedule | Only after a crisis or not at all | Regular checkups tied to life events and law changes |

| Support for family | Heirs must sort records alone | Heirs can call a known advisor who understands the plan |

Taking your next step

You do not need to wait for a crisis to act. You can start with three simple steps today. First, gather your recent tax returns and account statements. Second, write a short list of your top three goals for your family. Third, contact a trusted CPA and ask for help tying your goals to a clear estate plan.

Estate planning with a CPA does not remove all grief. It does remove confusion, guesswork, and many hidden costs. You give your loved ones a final gift. Clear direction, less conflict, and a calm path through a hard time.

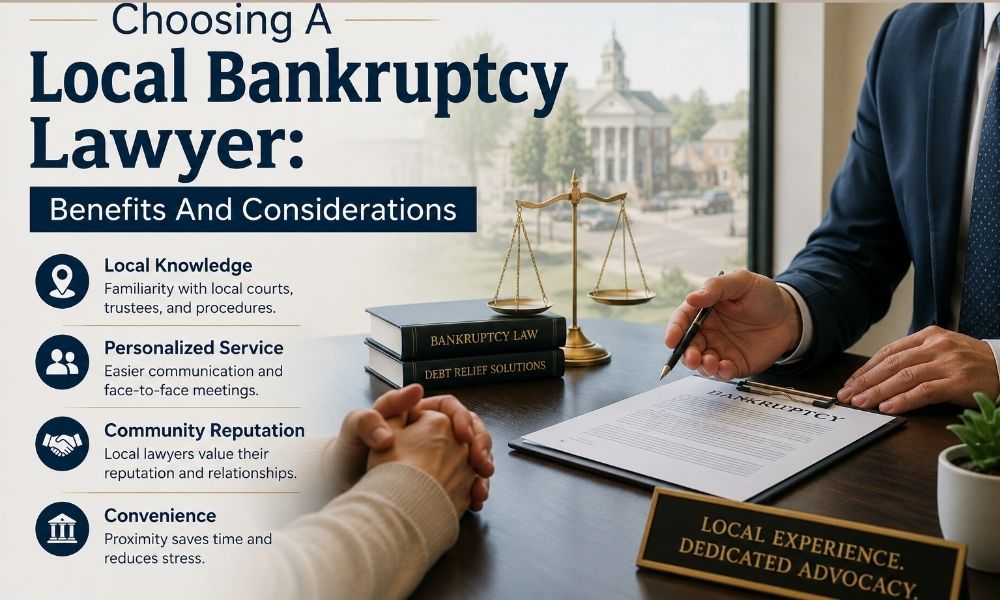

You might be feeling like your financial life is divided into a “before” and an “after.” Before the late notices, before the collection calls, before you started typing “bankruptcy help” into a search bar at midnight. Now you are here, wondering if hiring a local bankruptcy lawyer like Corey L. Mills is worth it, and afraid of making one more decision that could go wrong.end

That mix of shame, confusion, and urgency is very common. You may be thinking, “I never thought I would be in this position,” and at the same time, “I just want this to stop.” Because of that tension, it helps to slow down for a moment and look at what a nearby bankruptcy attorney actually does, when they help, and how to choose one wisely.

In simple terms, working with a nearby bankruptcy lawyer can make the process clearer, safer, and less overwhelming. You get guidance on whether bankruptcy is right for you, which chapter fits your situation, and how to protect as much of your income and property as the law allows. You also avoid common mistakes that can cost you time, money, or even the protection of the court.

So, where does that leave you right now? It means you do not have to decide everything today, but you can learn what to expect and what to look for in a local bankruptcy attorney, then take your next step with more confidence and less fear.

Why is choosing a nearby bankruptcy lawyer different from going it alone?

When you first think about bankruptcy, it can feel like walking into a foreign system where everyone speaks a different language. Terms like “automatic stay,” “means test,” and “exemptions” show up, and you are expected to make serious decisions based on rules you have never seen before.

If you try to handle the process yourself, you will be working inside a court system with strict deadlines, complex forms, and serious consequences if you miss something. The federal courts offer helpful education, for example, through Bankruptcy Basics from the U.S. Courts, yet information alone is not the same as a strategy tailored to your life.

That is where a local bankruptcy attorney can change your experience. A nearby lawyer understands not only federal bankruptcy law, but also how your particular court and trustees operate. For example, a Massachusetts filer can look at this guide to the Massachusetts bankruptcy court and see that each court has its own procedures, expectations, and local rules. A local lawyer works with those rules every day, which can keep your case smoother and less stressful.

So what happens if you choose to go alone or with someone who is not familiar with your court? You may misjudge which chapter to file under. You may claim the wrong exemptions and risk losing property you could have kept. You might overlook documents the trustee will ask for, which can delay or even threaten your case.

What emotional and financial challenges does a local bankruptcy lawyer help with?

Money problems rarely show up in just one area of life. They affect your sleep, your relationships, your work, and your sense of security. Because of that, choosing a local bankruptcy lawyer is not only a legal decision. It is also an emotional one.

Imagine this first scenario. You are behind on credit cards, medical bills, and maybe a personal loan. Collection calls are constant. You do an online search and find general information about bankruptcy, including examples from the New York Eastern District Bankruptcy Court’s learning resources. The information is helpful, but your questions are specific. Can you keep your car? What happens to your co-signer? Will your wages still be garnished? A local lawyer can sit with you, look at your income, debts, and assets, and answer those questions in plain language.

Now, a second scenario. You own a small business, and personal debts are tangled up with business obligations. You might be worried that filing for bankruptcy means losing everything you’ve built. A nearby bankruptcy attorney can explain how different chapters affect business owners and help you see whether there are non-bankruptcy options, or whether a reorganization or liquidation is the better path.

Because of these very real worries, it is easy to either rush into hiring the first person you find or avoid calling anyone at all. Both reactions are driven by stress, not by good information. The goal is to give yourself room to ask questions, compare options, and understand how a local bankruptcy lawyer can reduce risk and give you a clearer plan.

What are the real benefits and tradeoffs of local legal help?

To make this less abstract, it helps to compare three common paths. Handling a case yourself, using a non-local or low-contact service, or choosing a nearby bankruptcy lawyer who practices in your court.

| Option | Typical Benefits | Common Risks | Best Fit For |

|---|---|---|---|

| Do it yourself (no lawyer) | Lowest up-front cost. Full personal control of filings. | High chance of paperwork errors. Risk of losing non-exempt property. Stress of dealing directly with creditors and the court. | Very simple cases with little property and comfort reading legal instructions closely. |

| Non local or low contact service | Some guidance on forms. Often lower fees than full representation. | Limited knowledge of your specific court. Less personal attention. Harder to get help with emergencies or complicated issues. | People who mainly want help filling out forms and have straightforward situations. |

| Choosing a local bankruptcy lawyer | Familiar with local judges and trustees. Tailored advice on exemptions and chapter choice. Representation at hearings. Help dealing with creditors. | Higher cost than doing it yourself. Need to spend time choosing the right person. | Most people with mixed debts, property to protect, or any uncertainty about the process. |

There is no single right path for everyone. Still, for many people, working with a nearby bankruptcy attorney reduces risk and emotional strain enough that the legal fee feels like part of the solution, not an extra burden.

If you are deeply worried about cost, it may help to know that some courts and organizations maintain lists of low-cost or free legal help. For example, the District of Columbia Bankruptcy Court offers information on how to find an attorney, sometimes at no cost. Many areas have similar resources through legal aid offices or bar associations. A local lawyer can often point you toward payment plans or alternatives if traditional fees are out of reach.

What practical steps should you take before you choose a lawyer?

It is easy to feel frozen at this stage. You know you need help, but you are not sure what to do first. Here are three concrete steps you can take right away that do not require any commitment to file.

- Get clear on your financial picture in simple terms

Before you talk to any attorney, gather a short list of information. This does not have to be perfect or detailed. Aim for:

- A rough total of what you owe and to whom, including credit cards, medical bills, personal loans, taxes, and any judgments.

- Your average monthly income from all sources.

- Your regular monthly expenses like rent or mortgage, utilities, food, insurance, and car payments.

- A list of property you own that matters to you, such as your car, home, retirement accounts, or tools you use for work.

This simple snapshot helps any bankruptcy lawyer give you more accurate guidance during an initial conversation, and it helps you feel less scattered when you describe your situation.

- Talk to at least two local bankruptcy attorneys before deciding

You are not “bothering” anyone by asking questions. Initial consultations are often free or low-cost, and they are part of how attorneys build their practice. Aim to speak with at least two nearby lawyers and compare how you feel with each one.

During those conversations, you can ask:

- How many bankruptcy cases do they handle in your court each year?

- Whether they see any red flags or special issues in your situation.

- What their fee covers and what it does not.

- How they prefer to communicate, such as phone, email, or in-person meetings.

Pay attention not only to the answers, but to how you feel. Do you feel rushed or judged? Or do you feel heard and informed? That feeling matters more than many people realize, especially as you move through a process that can already feel exposing.

- Use trusted education resources while you consider your options

While you are deciding whether to hire a nearby bankruptcy attorney, you can also educate yourself using reliable, court-backed sources. These do not replace legal advice, but they help you understand the basic structure so you can ask better questions.

You might start with the federal courts’ Bankruptcy Basics overview to understand what chapters exist and what they do. If you are in a specific area, check your local bankruptcy court’s website for guides, such as the Massachusetts pro se guide or the learning section for the Eastern District of New York. Reading these resources while you talk with attorneys can help you feel more grounded and less at the mercy of a confusing system.

How can you move forward with more peace and less fear?

Financial trouble has a way of making people feel trapped and alone, yet you are far from alone in this. Many people have stood where you are standing now, unsure whether to reach out for help, worried about judgment, and afraid of one more bill. The truth is that talking with a nearby bankruptcy attorney does not lock you into filing. It simply gives you clearer choices.

As you decide what to do, remember this. You are allowed to ask questions. You are allowed to protect your peace of mind. You are allowed to choose support instead of facing creditors and court rules by yourself.

Your next step does not have to be dramatic. It can be as small as gathering your bills into one folder, reading a short court guide, or calling a local office to schedule a conversation. Each of those actions moves you out of fear and toward a plan.

You have already done something hard by seeking information. From here, you can keep going one step at a time, and with the right guidance, you can reach a more stable and livable financial future.

Choosing who handles your taxes is a hard decision. You want someone who protects you, guides you, and does not miss a single detail. A general accountant can record numbers. A CPA carries deeper training, testing, and strict licensing. That difference can protect your money, your business, and your sleep. This blog explains four clear advantages of hiring a CPA instead of a regular accountant. You will see how a CPA can stand up for you with the IRS, plan for your future tax bills, support major life changes, and keep you inside the law. You will also see how local knowledge matters. For example, Pasadena CPAs understand California rules that can trip people up. By the end, you will know what to ask, what to expect, and how to choose the right person to trust with your financial life.

1. Stronger training and licensing

You trust someone with your tax records. That trust should rest on clear proof. A CPA meets strict education rules, passes a tough exam, and holds a state license. A general accountant does not need this license.

CPAs must also complete regular education every year. You get someone who keeps up with new tax laws and reporting rules. That helps you avoid mistakes that lead to bills, letters, or audits.

The National Association of State Boards of Accountancy explains common CPA standards at this page. You can review those rules and see how they differ from basic accounting work.

Here is a simple comparison.

| Feature | CPA | General Accountant

|

|---|---|---|

| State license required | Yes | No |

| Uniform CPA Exam | Required | Not required |

| Continuing education | Required by law | Optional |

| Audit financial statements | Allowed | Not allowed |

| IRS representation rights | Unlimited | Limited |

You would not let an unlicensed driver take your family on a long trip. In the same way, you should expect real proof that your tax adviser meets strict standards.

2. Stronger protection during IRS problems

Letters from the IRS can shake any person. A past return might have an error. A form might be missing. A notice might claim that you owe more than you can pay.

CPAs can stand in front of you during these hard moments. The IRS grants CPAs full rights to represent you in audits, payment plans, and appeals. A general accountant has narrow rights. That gap matters when pressure rises.

A CPA can

- Review letters and notices and explain them in plain words

- Talk with the IRS for you so you do not face calls alone

- Help set payment plans if you owe taxes

- Correct past returns when needed

The IRS explains who can represent you here. That page lists CPAs along with attorneys and enrolled agents. You gain someone the IRS already recognizes.

This protection supports you during tax audits. It also encourages better records from the start, because CPAs know what an examiner will ask.

3. Better planning for life changes

Taxes do not sit still. Your life changes. Your tax needs change with it. Marriage, divorce, a new child, a home purchase, or a move across state lines can all change your tax bill.

A CPA can plan ahead with you. You do not wait for tax season. You talk before big choices. That way you see the trade offs and choose your path with clear eyes.

Common life events where a CPA helps include

- Starting a small business or side income

- Buying or selling a home

- Paying for college

- Planning for retirement income and Social Security timing

- Receiving an inheritance

You gain three main benefits. You lower surprise tax bills. You reduce the chance of missing credits. You align your money choices with your personal goals.

A general accountant often focuses on past records. A CPA focuses on both past and future. That forward view gives your family more control.

4. Stronger trust and legal duty

Trust is not soft. It rests on clear duties. CPAs must follow a strict code of conduct and can lose their license if they abuse that duty. That pressure protects you.

CPAs must

- Protect your private records

- Refuse to sign returns they believe are false

- Disclose conflicts of interest

This duty shapes daily choices. A CPA is less likely to suggest risky moves that might look good for one year then harm you later. You get advice that respects both your short term needs and your long term safety.

That sense of duty also supports family talks. You can bring a spouse or older child to meetings. You can ask hard questions about debt, savings, or retirement. You can expect honest, direct answers.

How to choose the right CPA for your needs

Once you decide to hire a CPA, you still need to choose the right person. You can use a simple rule of three.

First, check the license. Your state board of accountancy keeps records of active licenses and any public discipline. You can search those records and confirm that the person you meet is in good standing.

Second, review the focus of the CPA. Some focus on large companies. Some focus on small business owners. Others focus on families and retirees. Choose someone who often works with people like you.

Third, ask clear questions.

- How often do you handle IRS letters and audits

- How will we stay in touch during the year

- What records do you need from me

- How do you set your fees

You should leave the first meeting with three feelings. You should feel heard. You should feel informed. You should feel calmer than when you walked in.

Conclusion

Your tax returns shape more than one date on the calendar. They touch your savings, your home, your business, and your sense of safety. A general accountant can record what already happened. A CPA can protect you, plan with you, and stand up for you when things go wrong.

By choosing a CPA, you gain stronger training, full IRS representation, better planning for life changes, and a higher duty of care. Those four advantages give you and your family steadier ground. You deserve that level of support when you place your financial life in someone else’s hands.

You work hard for your money. Regular talks with a CPA protect it. Many people only call during tax season. That choice often leads to missed chances, surprise bills, and quiet stress that grows all year. Ongoing check ins with a trusted CPA in Sarasota, FL give you steady guidance when laws change, when life shifts, and when your plans feel unclear. You gain clear answers before problems grow. You also gain simple steps you can act on right away. Year round support can cut tax shocks, stop small mistakes, and uncover savings you might never see alone. It can also keep your records clean so audits feel less scary. This blog explains four strong advantages of regular CPA consultations throughout the year so you know what to expect, what to ask, and how to use that support to protect your income and your peace of mind.

1. You stay ahead of tax changes

Tax rules shift often. You feel the cost when you learn about a change after it hits your wallet. Regular talks with a CPA help you adjust before that happens.

The IRS updates forms, limits, and credits each year. You can track some of this on the IRS Newsroom page. Yet it is hard to match each change to your own life. A CPA listens to your story and points to what matters for you, your spouse, or your kids.

During the year, you can use check-ins to review:

- New credits for children, students, or energy upgrades

- Changes to retirement contribution limits

- Shifts in rules for small side jobs or gig work

Each talk gives you time to adjust paychecks, update forms at work, and set up better record-keeping. You do not scramble in March. You walk into tax season ready.

2. You cut surprise tax bills and penalties

Large tax bills do more than drain savings. They create shame, fear, and tension in your home. Regular CPA visits help you see those shocks coming while there is still time to act.

Here is a simple comparison of one tax season visit and year-round support.

| Approach | What usually happens | Risk to you

|

|---|---|---|

| One visit at tax time | CPA reports what already happened that year | Higher chance of a big bill or missed refund |

| Quarterly check ins | CPA reviews income, withholdings, and life changes | Lower chance of surprise taxes or late fees |

| Monthly or life event check ins | CPA adjusts plan when you change jobs, move, or start a side job | Strong control of cash flow and fewer shocks |

During the year, your CPA can help you:

- Raise or lower tax withholding on your paycheck

- Set up or change estimated tax payments if you are self-employed

- Respond fast to IRS letters instead of letting fear grow

That guidance helps you avoid late payment penalties and interest. It also lowers stress in your home and gives you a clear plan when money feels tight.

3. You use life changes to your benefit

Life does not follow the tax calendar. You marry, divorce, move, or care for aging parents when life demands it. Each change affects your money and your taxes. Regular CPA talks help you use those shifts instead of feeling pushed by them.

Three common life changes show why steady support matters.

- New job or raise. Your income climbs. Without a plan, your tax bill can spike. A CPA can help you adjust your W 4, pick the right benefits, and start or grow retirement savings.

- Birth or adoption. A new child brings love and cost. It can also bring tax credits. Your CPA can explain how to claim a child, use the Child Tax Credit, and track care or education costs over time.

- Starting a side job or small business. Extra income feels good. Poor record-keeping turns that joy into dread. A CPA can set up a simple system for tracking income and costs so tax time is clear and clean.

You can read basic guidance on life events and taxes from the IRS at the IRS Tax Topic 304 page. A CPA turns that general advice into steps that fit your life. You then face each change with less fear and more control.

4. You build a steady plan for savings and goals

Taxes and long-term goals are tied. Regular CPA visits help you see that link. You can then use the tax code to support the life you want, not just to avoid trouble.

During ongoing talks, a CPA can help you:

- Choose between traditional and Roth retirement accounts

- Plan for college costs for your children or grandchildren

- Prepare for long-term care needs for yourself or your parents

The U.S. Securities and Exchange Commission and other agencies share basic saving tips, yet those guides are broad. Your CPA looks at your income, family size, debt, and health needs. Then you work together to set three clear pieces.

- A short-term plan for the next year

- A mid-term plan for the next three to five years

- A long-term plan for retirement and aging

Each visit lets you check progress, adjust for new facts, and protect both your goals and your sense of safety.

Putting regular CPA consultations to work

Regular CPA talks are not a luxury for the wealthy. They are a shield for everyday families who want less fear and more control. You can start small.

First, set one meeting now, not during tax rush. Bring pay stubs, last year’s return, and a list of worries. Second, ask how often you should meet based on your job, family, and side work. Third, commit to the schedule. Treat it like a medical check-up for your money.

Steady support from a CPA will not remove every hard thing in life. It will give you clear sight, fewer shocks, and more room to breathe. You deserve that peace all year, not just in tax season.

BMW Wheels and Alloys: Sizes, Fitments and What to Check Before Buying Used

BMW Wheels and Alloys: Sizes, Fitments and What to Check Before Buying Used

Can Wisdom Teeth Cause Headaches? Dental Signs, Causes, and Treatment Options

Grace Fan Devito: The Quiet Power Behind Danny DeVito’s Daughter 2024

The Rise of AI in Fashion: How Technology is Redefining Style in 2025

Make1M.com Luxury Watches: Timeless Elegance Meets Financial Freedom

-

ENTERTAINMENT2 years ago

ENTERTAINMENT2 years agoGrace Fan Devito: The Quiet Power Behind Danny DeVito’s Daughter 2024

-

FASHION2 years ago

FASHION2 years agoThe Rise of AI in Fashion: How Technology is Redefining Style in 2025

-

FASHION2 years ago

FASHION2 years agoMake1M.com Luxury Watches: Timeless Elegance Meets Financial Freedom

-

CELEBRITY2 years ago

CELEBRITY2 years agoLinda Susan Agar: A Visionary Leader Shaping the Future of the Technology Industry 2024

-

CRYPTO2 years ago

CRYPTO2 years agoeCrypto1.com Crypto Wallets: The Ultimate Guide to Secure and Efficient Cryptocurrency Storage 2025

-

CELEBRITY2 years ago

CELEBRITY2 years agoThe Life and Legacy of Harlow Andrus: A Journey of Heritage and Inspiration 2024

-

CELEBRITY2 years ago

CELEBRITY2 years agoThe Viral “Emiru Handbra” Moment: How It Became a Stunning Social Media Sensation in 2024

-

CELEBRITY2 years ago

CELEBRITY2 years agoDavid Nehdar: The Private Life and Success of Lacey Chabert’s Husband 2025